Hello, I'm Ryuta Hamamoto from TIMEWELL.

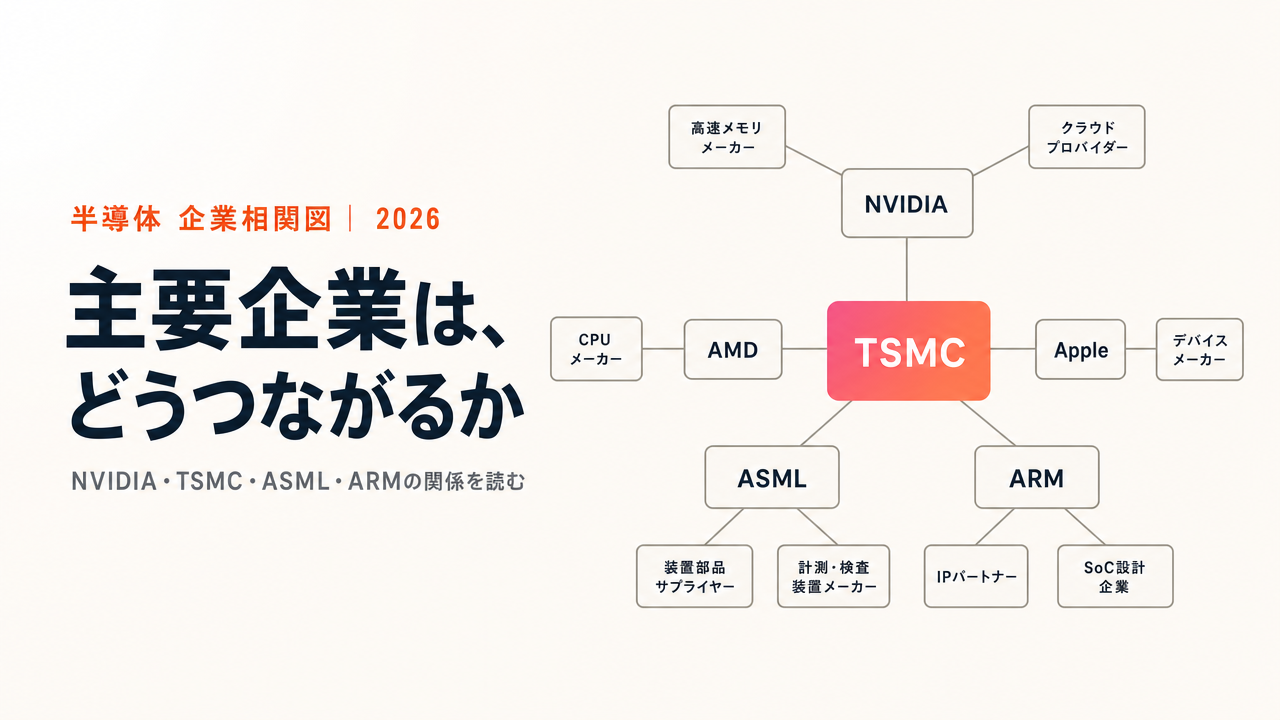

In A Beginner's Guide to the Semiconductor Industry's Structure, we walked through the division of labor across design, manufacturing, equipment, materials, and memory. This time, let's fill in the actual company names that play those roles and draw a single relationship map.

Picture a soccer player relationship chart. Who is the ace, who is the playmaker, and who is the unseen support working in the background? Once you understand the positions and the relationships, the whole match looks different. Semiconductors work the same way. Once you grasp how the players connect, you can read how a single piece of news ripples through the entire industry. Along the way, I'll plant a few conversation starters too, like "why did Intel fall?" and "who is the mystery $10 billion customer?"

The Two Star Designers, and the Unseen Support: ARM

The companies grabbing the most attention right now are the ones that design chips. The ace, needless to say, is NVIDIA. It built an overwhelming position in GPUs (chips that excel at massive parallel computation) for AI, and in October 2025 its market capitalization became the first in the world to break $5 trillion. That makes it the largest company on the planet. Chasing it head-on is AMD, a longtime rival. In soccer terms, they are the two strikers racking up the goals.

What's easy to overlook here is ARM, which props them up from below. ARM doesn't make a single chip, but it lends out the intellectual property that serves as the "basic recipe" for circuit design. Nearly every processor inside a smartphone is built on ARM's design philosophy, and ARM earns a royalty every time a chip is sold. It never steps onto the main stage, yet it is like the unseen figure dressed in black who writes the rulebook for the entire pitch. SoftBank Group owns about 90% of ARM, which means this is hardly someone else's problem for Japan.

Apple is its own peculiar case. It designs the chips for the iPhone and Mac in-house, and their performance is beyond question, but it never sells those chips to anyone. NVIDIA sells to the world; Apple keeps everything in-house. The fascinating part is that two companies that both "design chips" can take stances that are complete opposites.

Take AI-driven development all the way to production

WARP is a hands-on program for teams who want more than headlines. Former enterprise DX and data strategy leads work alongside you until it runs.

NVIDIA's Sheer Dominance, by the Numbers

NVIDIA's strength becomes obvious the moment you line up the numbers. In a single quarter at the start of 2026, revenue was about $81.6 billion, of which the data center segment alone was about $75.2 billion. Meanwhile, rival AMD's total company-wide revenue over the same period was about $10.2 billion. In other words, NVIDIA's data center segment alone was roughly seven times the entire revenue of AMD. The gap in raw muscle in AI silicon is still overwhelming.

The product roadmap is just as aggressive. From today's Blackwell (with the GB200 and similar integrated racks holding 72 GPUs as the flagship), it plans to refresh the generation every year: a next-generation Rubin carrying HBM4 in the second half of 2026, and Rubin Ultra, which links those together, in 2027. But AMD isn't staying quiet either. With a rack-scale product called "Helios" launching in the second half of 2026, it is said to surpass NVIDIA in memory capacity and to take it on directly at rack scale for the first time. NVIDIA's true moat, though, lies less in the chips themselves than in the stronghold of its development software, CUDA. How AMD chips away at that is where the contest will be decided.

The Backstage Player Broadcom and the "Mystery $10 Billion Customer"

Let me introduce one unexpected dark horse here: Broadcom. It isn't a company that sells flashy brand-name chips, but it plays a behind-the-scenes role, co-designing dedicated custom chips (called AI ASICs) for AI companies like Google, Meta, and even OpenAI and Anthropic. It grew rapidly by catching the true feelings of massive customers who think, "We'd rather not be entirely dependent on NVIDIA's expensive general-purpose GPUs; we want cheaper chips optimized for our own workloads."

There's a telling episode. In 2025, Broadcom announced it had landed an order on the scale of $10 billion from a "fourth customer," and the industry buzzed over who it could be. The reveal came in December 2025. CEO Hock Tan disclosed that the mystery customer was Anthropic. The companies running at the very front of AI are the ones that want their own chips, and Broadcom is the one company drawing that whole trend toward itself.

Why Did the King, Intel, Fall?

Few industries see fortunes rise and fall this dramatically, and the symbol of it is Intel. It once ruled the PC era as "Wintel," the vertically integrated king that handled everything in-house from design to manufacturing. So why did it fall? There are "three failures" worth telling as conversation pieces.

The first, in 2007. When Apple approached Intel about manufacturing chips for the iPhone, Intel turned it down, saying the volumes would be too small. Apple had no choice but to turn to ARM's design, and that decision shaped the entire map of today's smartphone semiconductors. The second was being overtaken by TSMC in manufacturing technology. Its own miniaturization slipped again and again, while rival AMD used TSMC's leading edge to leapfrog it on performance. The third was arriving late to the AI wave. The starring role in GPUs was completely seized by NVIDIA.

As a result, Intel posted a massive loss of about $18.8 billion in 2024. In March 2025 it brought in industry veteran Lip-Bu Tan as its new CEO, and that same year the US government invested about $8.9 billion to take roughly a 9.9% stake, while NVIDIA put in $5 billion and SoftBank $2 billion, a situation once unthinkable. The former king, propped up by companies that used to rank beneath it, attempts a turnaround. The semiconductor map can be redrawn this completely in just a few years.

Tangled by Capital, Too: SoftBank, ARM, and the Web of Investment

Semiconductor companies are entangled not only in design and manufacturing but also in money, that is, in capital. The relationship worth knowing as a Japanese reader above all is the one between SoftBank Group and ARM. SoftBank acquired ARM in 2016, and even after relisting it in the US in 2023, it has held on to about 90% of the shares. As noted, ARM makes no chips; it lends out the "basic recipe" for design and collects a royalty (a few percent of the sale price) every time a chip is sold. It's a passive-income-style premium business where revenue ticks up steadily however many smartphones sell. And it's been reported that this same ARM is now making its own chip for the first time in its history, with Meta as its first customer. The figure in black who used to write the rulebook is now stepping onto the pitch itself.

SoftBank itself keeps betting heavily on AI silicon. It acquired Ampere, which makes server CPUs, invested $2 billion in the recovering Intel, and has poured tens of billions of dollars cumulatively into OpenAI. What's more, the foundation of data center CPUs, whether NVIDIA's Grace, Amazon's Graviton, or Microsoft's Cobalt, is in every case ARM. In other words, a Japanese company holds one of the most important rules of the AI era. Looking at the market as a whole, the global semiconductor market in 2025 swelled to roughly $800 billion, of which AI-related now accounts for about a third. That's explosive growth in just one or two years.

And in the world of memory, a satisfying upset took place. The protagonist is South Korea's SK Hynix, long stuck in second place. The former king, Samsung, once judged that "HBM is a niche" and eased off its development; SK Hynix, meanwhile, kept quietly honing the technology. When the AI boom arrived and NVIDIA demanded huge volumes of HBM, the only one that could mass-produce it immediately was SK Hynix. The result: in 2025 it finally surpassed Samsung in operating profit. A complacent king and a prepared runner-up. It's a prime example of how the seismic shift of AI flipped the corporate pecking order.

All Roads Lead to TSMC, and TSMC Bows to ASML

The design companies named so far share one thing in common. NVIDIA, AMD, Apple, Broadcom—none of them owns a fab. Nearly all of them outsource manufacturing to Taiwan's TSMC. This is the center of the relationship map, a state of affairs where "all design roads lead to TSMC."

An interesting dynamic plays out here. Because TSMC's manufacturing capacity is finite, customers fight over it. In 2025, NVIDIA finally overtook Apple to become TSMC's largest customer (a revenue contribution of about $23.4 billion, 19% of the total). At the same time, Apple had moved early to lock up more than 50% of TSMC's 2nm (leading-edge) manufacturing capacity for 2026. In other words, there's a two-tier structure: NVIDIA is the top customer by revenue, while Apple holds the priority slots on the leading-edge node. So the leading-edge manufacturing capacity that can actually be directed at AI is smaller than it looks. This is a hidden cause of the supply crunch.

Even TSMC bows to the Netherlands' ASML (the only company in the world that makes EUV lithography machines, introduced last time) and to the three memory makers (SK Hynix, Samsung, and Micron). In memory especially, the upset I described took place. SK Hynix, long in second, was first to reach mass production of HBM for AI, and in 2025 it finally surpassed Samsung in operating profit. Japan's Kioxia, riding NAND demand for AI, climbed to the top of the domestic market by market capitalization.

When you pull all of this into a single picture, the industry's "pressure points" stand out clearly. Leading-edge manufacturing rests on one company, TSMC; EUV equipment on one company, ASML; AI-grade memory on just three companies. In peacetime this concentration is a source of efficiency, but in a crisis it flips into a fatal weakness. And it is precisely these pressure points that governments around the world are desperately trying to corral. Why does a story about a single company become a matter of national security? We dig into the answer in the next piece, The Geopolitics of Semiconductors and a Taiwan Contingency.

Note: Figures on revenue, market capitalization, and customer relationships draw on the IR materials of NVIDIA, AMD, and Broadcom, along with CNBC, companiesmarketcap, and Tom's Hardware; details on Intel's investments and CEO change draw on company announcements and reporting from outlets such as Manufacturing Dive (all from 2025 to 2026).