Hello, I'm Ryuta Hamamoto from TIMEWELL.

Right now, the smartphone in your hand contains a chip the size of a grain of rice packed with tens of billions of switches. In the latest AI chips, that count exceeds 200 billion. And it takes three months to build one, walking through as many as 1,400 process steps. This "grain of sand" we use without a second thought is, in fact, among the most fiendishly complex industrial products humanity makes.

In The Big Picture of Semiconductors and Economic Security, I explained that no single company can make a leading-edge semiconductor on its own, and that companies around the world divide up the work. In this article, I want to go one level deeper into how they are made and who makes them. Technical terms will come up, but I'll explain every one of them through cooking and cookies, so there's no need to brace yourself. By the time you finish, semiconductor news will feel three-dimensional, and you'll probably catch yourself wanting to tell someone about it.

What Exactly Is a Semiconductor, and Why Is It "the Oil of Our Era"?

A semiconductor is a material whose properties sit between metals that "conduct" electricity and insulators that "don't"—and silicon (the main component of sand) is the star player. By exploiting this halfway behavior, you can build, at microscopic scale and in vast numbers, switches that turn electricity on and off—in other words, the 0s and 1s. That is what we call a "semiconductor chip."

How microscopic? When the Intel 4004 launched in 1971 as the world's first commercial microprocessor, it had a mere 2,300 switches (transistors). NVIDIA's 2024 AI chip, Blackwell, has 208 billion. That's roughly 90 million times more in half a century. Cramming more than 1,700 times the population of Japan's worth of switches onto an area about the size of a postage stamp—does that convey just how insane the scale has become?

The faster and more energy-efficiently these switches run, the smarter AI and smartphones become. That's why the whole world fights over semiconductors. Just as oil was the lifeblood of 20th-century industry, semiconductors have become the lifeblood of the 21st. That's why they're called "the oil of our era."

Take AI-driven development all the way to production

WARP is a hands-on program for teams who want more than headlines. Former enterprise DX and data strategy leads work alongside you until it runs.

A Chip Is a Three-Month, 1,000-Step Epic

So how is that grain of sand actually made? Let me trace it through roughly seven stages, using a cooking analogy.

It starts with wafer production. You melt ultra-high-purity silicon at about 1,400°C, dip in a seed crystal, and slowly rotate while pulling it up—and an enormous "pillar of rock candy" grows, with its atoms all neatly aligned. Slice that into thin discs and you get wafers, the foundation of a chip. Next comes the hardest part: lithography (photolithography). You shine light through a circuit "master," shrink it through a lens, and burn the pattern into the photosensitive coating on the wafer—essentially silkscreen printing. At the leading edge, this uses a special kind of light called EUV (extreme ultraviolet) with a wavelength of 13.5nm, and the way that light is created is astonishing. In a vacuum, droplets of molten tin are blasted out 50,000 times per second, and two powerful laser pulses are fired into each one to turn it into plasma, squeezing out the 13.5nm light. A process straight out of science fiction is, at this very moment, running in factories.

After the pattern is burned in, etching carves away the unwanted parts like a copperplate engraving, ion implantation drives impurities to a targeted depth to fine-tune the material's properties, and deposition coats on a fresh layer. This cycle of "print, carve, implant, stack" is repeated dozens of times, building the circuit up in three dimensions. That is what "more than 1,000 total process steps" really means. Finally, dicing cuts the wafer into individual pieces like breaking apart a bar of chocolate, and packaging seats each one in a case with terminals—and at last you have a usable component.

From sand to here takes about three months. When you buy a smartphone, picture the single chip inside it having been born three months earlier in a Taiwanese factory—doesn't that shift your perspective a little?

"2nm" Isn't Actually a Measurement

A term you'll always run into in semiconductor news is "2nm" or "3nm." Many people assume "the circuit is 2 nanometers wide," but strictly speaking, that's wrong.

It's true that up through the 1990s, this number roughly matched the actual processing dimensions. But as miniaturization advanced, that correspondence broke down, and today even the "2nm" generation has actual circuit spacing of about 45nm. That's a completely different order of magnitude from the "2" in the name. In other words, today's node names are not physical dimensions but brand names and grade labels that signal "this is more advanced than the previous generation." Picture clothing sizes "M" and "L." They may once have reflected actual measurements, but now they're just labels for "roughly this level of performance." Just knowing this dramatically sharpens the resolution of the news you read.

By the way, the famous "Moore's Law" (chip performance doubles every two years) is now on its deathbed. NVIDIA CEO Jensen Huang has flatly declared "Moore's Law is dead," while TSMC counters that "it has slowed but isn't dead." What they share is the recognition that "miniaturization continues, but it no longer gets cheaper." 2nm is hard because it requires simultaneously overhauling three things at once: the transistor structure, the way power is delivered, and the lithography equipment. The closer you get to the leading edge, the more both technology and cost feel like climbing a cliff.

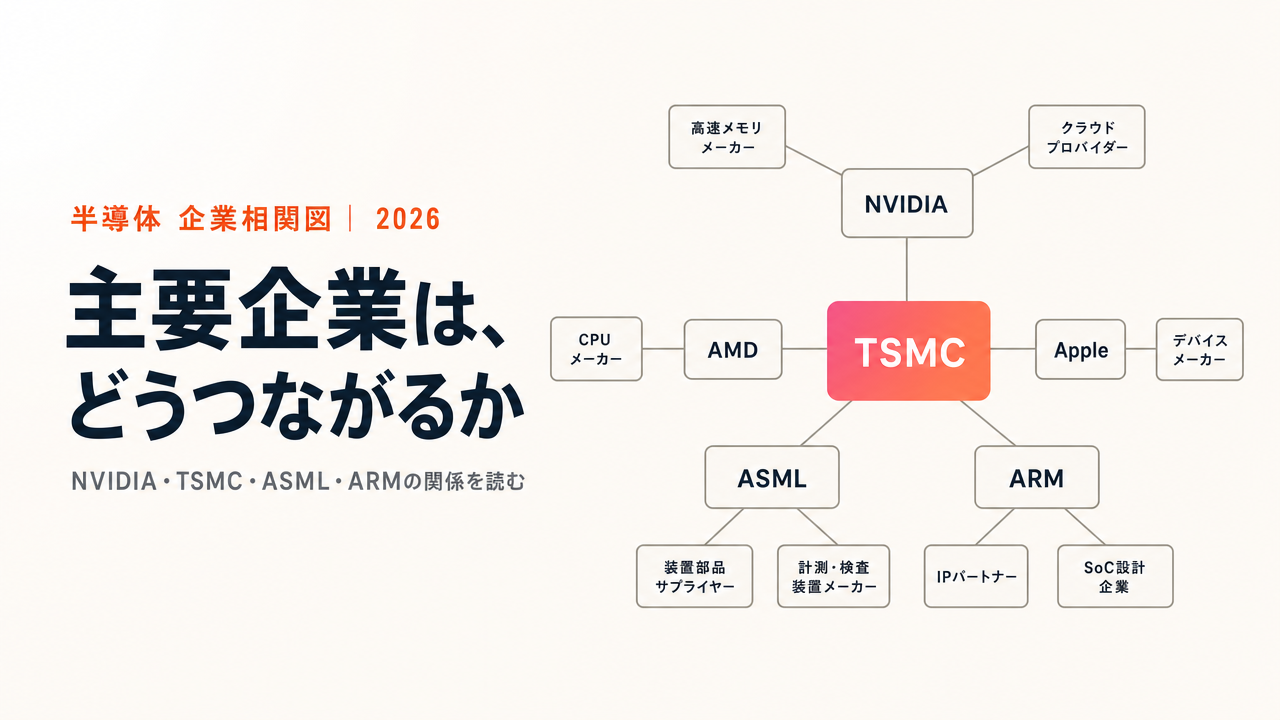

No One Company Can Make It—the Chain of Division, and "All Roads Lead to TSMC"

Here's the heart of the industry's structure. A leading-edge semiconductor absolutely cannot be made by one company alone. Like a full-course meal at a high-end restaurant, the roles are cleanly divided.

The UK's ARM provides the intellectual property that serves as the "base recipe" for circuit design; design-only companies like NVIDIA, Apple, and AMD (called fabless—as in fab, meaning factory, plus less, meaning without) use it to design chips. Since they own no factories, they outsource manufacturing to Taiwan's TSMC. And TSMC, in turn, can do nothing toward etching leading-edge chips without the lithography machines made by the Netherlands' ASML—and those factories run on top of silicon wafers, of which Japanese companies like Shin-Etsu Chemical and SUMCO hold roughly 60% of the world's supply. In cooking terms: ARM is the base recipe, NVIDIA and the others are the chefs planning the menu, TSMC is the only kitchen on Earth that can finish this fiendishly hard dish, ASML is the special oven that can only be installed in that one kitchen, and the Japanese players are the suppliers of the finest ingredients.

In this chain, the one that matters overwhelmingly is TSMC. The blueprints of design companies the world over ultimately converge on this single kitchen. Its foundry (contract manufacturing) market share exceeds 70%, and at the leading edge it holds more than 90%. Borrowing from ancient Rome's "all roads lead to Rome," you could say "all designs lead to TSMC." A telling sign: in 2025, NVIDIA overtook Apple to become TSMC's largest customer. Revenue from NVIDIA reached roughly $23.4 billion, about 19% of TSMC's total. The world's finest manufacturing capacity, once reserved for smartphones, was now being used for AI. The changing of the guard in semiconductors showed up clearly on TSMC's order book.

ASML, the Industry's "Pickaxe Seller," and Japan's Hidden Dominance

Even TSMC has someone it can't argue with: the Netherlands' ASML. The only company in the world that can build the EUV lithography machines essential for cutting-edge chips is this one. Its share is, literally, 100%. A single standard machine costs hundreds of millions of dollars, and the latest High-NA model runs to several hundred million more. In size, it's about as big as a city bus.

This calls to mind the old line: "The people who made the most money in the gold rush weren't the ones who dug for gold—they were the ones selling pickaxes and jeans." In a semiconductor industry riding the AI boom, the one company on Earth selling that very pickaxe is ASML. No matter how dazzling NVIDIA or TSMC may be, if ASML won't sell the equipment, not a single leading-edge factory can move an inch. Ordinary people know the names NVIDIA and Apple but not ASML. "The most important company in the world that you've never heard of"—that's a line guaranteed to land at a dinner party.

And does Japan have no part to play? Quite the opposite. In manufacturing equipment, Tokyo Electron is the world's third largest, holding nearly 90% global share in the tools that deposit the films circuits are built from; in materials, Japan's two companies Shin-Etsu Chemical and SUMCO supply roughly 60% of the world's silicon wafers, and when it comes to photoresist (the photosensitive coating essential for burning in circuits), Japanese players hold roughly 90% of the world's supply. In other words, semiconductors are built on a beautifully orchestrated international division of labor: "America designs, Taiwan manufactures, and the Netherlands' equipment and Japan's materials hold it all up." Japan doesn't stand in the spotlight, but it controls the underpinnings of semiconductors.

HBM, the Heart of AI, and CoWoS, the Final Checkpoint

Finally, let me introduce two players that suddenly leapt to the lead in the AI era.

One is HBM (High Bandwidth Memory). This is a specialized component made by stacking memory in many layers so data can be exchanged all at once. No matter how brilliant a GPU is, if it's slow at flipping through the documents at hand, it can't deliver its full ability. HBM is like a secretary sitting beside that genius, flipping through the documents at blistering speed and handing them over. Only three companies can mass-produce it—South Korea's SK Hynix and Samsung, and the U.S.'s Micron—and among them, SK Hynix is so short on supply that it says it's "sold out for years to come." It's a hidden winner of the AI boom.

The other is an unexpected bottleneck: CoWoS. This is TSMC's advanced packaging technology, the process of mounting the GPU itself and multiple HBMs tightly onto a single base and integrating them into one. Without it, an AI chip can't be completed. But because effectively only TSMC can mass-produce it at scale, you end up with the relationship: "the number of CoWoS units TSMC can process = the number of GPUs NVIDIA can ship." A high-end restaurant where the chefs and ingredients are all ready—but there's only one plating station. This is one of the real causes of the AI chip shortage. Japan's Kioxia, too, found its NAND memory selling like wildfire amid demand for data storage for generative AI, and in June 2026 it became the most valuable listed company in Japan by market cap.

Here's one more concept that's key to understanding the industry's economics: "yield." Yield is the proportion of working, good chips you can get from a single wafer. Picture baking cookies. If you fill the tray and bake, a few come out burnt—but the cost of running the oven for that tray doesn't change no matter how many burn. So the fewer that burn, the cheaper each edible cookie becomes. And the bigger each cookie is, the greater the loss when one burns. That's why the industry moved away from giant monolithic chips toward the "chiplet" approach of combining small chips like Lego. With a monolith, a single defect anywhere ruins the whole thing; with Lego, you just throw away the one defective block. In a world where building a leading-edge fab costs the equivalent of trillions of yen and designing a single 2nm chip alone costs about $700 million, a few percentage points of yield is the difference between heaven and hell.

By now you should be able to see that semiconductors are built from a division of roles—design, manufacturing, equipment, materials, and memory—and that the whole thing depends on two pressure points: TSMC and ASML. Next, I'll map out how the specific companies playing those roles compete with and depend on one another, in A Correlation Map of the Key Players. Once you understand the structure, you understand the balance of power. And once you understand the balance of power, you start to see why all of this becomes a matter of national concern.

References: Process step counts and timelines are from the Semiconductor Industry Association (SIA); TSMC's market share and individual company figures from TrendForce, CNBC, and companiesmarketcap; transistor counts and equipment prices from TechInsights, ASML, and Tom's Hardware; Kioxia's market cap from Nikkei (all based on reporting from 2025–2026).